On June 12, 2025, India’s Finance Ministry officially confirmed that no Merchant Discount Rate (MDR) will be imposed on Unified Payments Interface (UPI) transactions. This clarification comes after weeks of speculation that banks and fintech firms were lobbying to revive MDR fees—widely perceived as a catalyst for monetizing UPI. Here’s what this means for merchants, consumers, and the future of digital payments in India.

What is UPI and MDR?

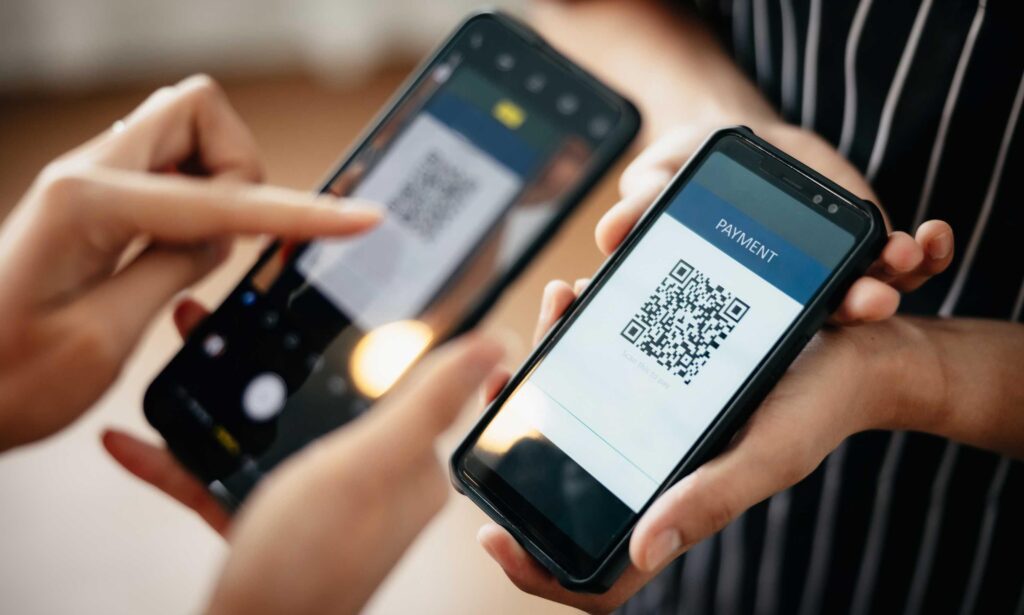

UPI, launched in April 2016 by the NPCI and regulated by the RBI, revolutionized digital payments with an easy peer‑to‑peer and peer‑to‑merchant interface via mobile apps.

MDR is essentially a service fee traditionally borne by merchants for processing digital payments commonly seen with credit/debit cards.

Until January 2020, MDR applied to RuPay and BHIM‑UPI transactions. But amendments to the Payments & Settlement Systems Act and Income‑Tax Act eliminated these charges to boost digital adoption.

Why the MDR-Free Stance?

In a post on X (formerly Twitter), the Finance Ministry labeled rumors about reintroducing MDR on UPI as “false, baseless and misleading,” worrying they’d create unnecessary fear among merchants and consumers.

Additionally, they reaffirmed ongoing support via incentive schemes like the ₹1,500 crore fund to promote RuPay and low-value BHIM‑UPI transactions—especially for small merchants .

What Led to This Clarification?

-

Banks and fintech lobbying: In early April, it was reported that authorities considered a 0.2–0.3% MDR on large UPI payments to help sustainable growth and investment in fintech.

-

Industry body pressure: The Payments Council of India had proposed reintroducing a 0.3% MDR on large-ticket UPI transactions, targeting merchants with annual GST turnover above ₹40 lakh.

With UPI volume nearing saturation (≈18.7 billion transactions and ₹25.1 lakh crore value in May), MDR was viewed by some as essential for monetization.

Impact on Fintech and Stock Markets

The MDR-free policy hit fintech stocks hard:

-

Paytm’s parent company One 97 Communications saw its shares slump ~10% intraday, closing ~8% lower following the statement—reflecting investor concerns over revenue loss.

-

Other fintechs like Mobikwik also saw declines amid uncertainty around UPI monetization strategies.

Many firms had raced to IPOs in 2025, banking on UPI-based revenues. The government’s stance removed a key income stream for them .

Benefits for Merchants & Consumers

-

Merchants: Continue to enjoy zero MDR on UPI, lowering overheads and encouraging digital acceptance—even among small, tier‑2/3 segment businesses .

-

Consumers: Face stable, hassle-free digital transactions without hidden costs.

-

UPI ecosystem: Sees sustained growth—May marked a 33% YoY rise in UPI volume and 41% in value.

-

Government: Signals strong commitment to creating a cashless India, aligning with broader financial inclusion goals.

What’s Next?

-

Monetization pivot: Fintechs may need to shift focus—from MDR to value‑added services like lending, insurance, subscriptions, and partnerships.

-

Possible split incentives: Some experts hint at limited MDR on large-ticket transactions, but Finance Ministry’s current stance blocks any such move for now.

-

IPO watch: Stakeholders will closely monitor fintech IPOs like PhonePe and Razorpay (2026), tracking their ability to pivot profit models.